Mastering Risk Management: Essential Steps to Protecting Your Business

Introduction

Running a business is an exciting and challenging venture. Whether you are a small business owner, a startup founder, or managing a large enterprise, risks are an inevitable part of your journey. From financial downturns to cybersecurity threats and operational disruptions, unforeseen events can significantly impact a business’s success and survival.

This is where risk management comes into play. Risk management entails identifying, assessing, and addressing potential threats to ensure the stability and growth of your business. It is not about avoiding risks entirely but about preparing for them and minimising their impact when they arise.

In today’s fast-paced and interconnected world, a sound risk management strategy is not optional. It is essential. Businesses that actively manage risks protect their assets and reputation and position themselves for long-term success in a competitive market.

This article discusses the fundamentals of risk management – what it is, why it matters, and how to implement it effectively. It helps you understand the meaning of risk management, the importance of risk management for business, and how to protect your business against uncertainties and confidently navigate challenges. Let’s dive in!

What is Risk Management?

According to ISO 31000, risk management entails coordinated activities to direct and control an organisation’s risk. This definition highlights risk management’s structured and systematic nature, emphasising its role as a critical component of good business governance. Risk management identifies, assesses, and addresses potential risks that could negatively impact an organisation’s operations, assets, reputation, or overall goals.

It entails identifying, evaluating, and addressing potential risks that could negatively impact an organisation, project, or individual. It is a proactive approach to dealing with uncertainties that businesses face, ensuring they are prepared to handle challenges effectively and recover quickly when things go wrong. It involves a systematic approach to understanding what could go wrong, evaluating the likelihood and impact of such events, and implementing measures to reduce, transfer, or accept risks. Moreover, businesses can prepare for future uncertainties by reflecting on the evolution of risk management and learning from history’s successes and failures.

The Goal of Risk Management

Risk management is crucial in safeguarding organisations and individuals against uncertainties while enabling informed decision-making. Risk management objectives are broad and interconnected. The primary goals of risk management include:

1. Minimise Uncertainty and Potential Losses: Risk management reduces the impact of unexpected events and uncertainties that could harm organisational goals. It ensures that potential threats are identified and addressed proactively. By mitigating risks, organisations can minimise disruptions and financial losses. For example, a manufacturing company exposed to supply chain risks can engage backup suppliers to reduce the impact of potential delays.

2. Protect Assets, Resources, and Stakeholders: Risk management protects an organisation’s physical, financial, and human assets. Risk management includes securing critical resources from theft, damage, or legal liabilities. It also protects stakeholders, including employees, customers, and shareholders. For instance, an organisation may adopt cybersecurity measures to protect sensitive customer data and prevent reputational damage.

3. Support Decision-Making with Risk-Informed Insights: Risk management enables leaders and managers to make informed decisions by understanding potential risks and their implications. A structured risk management approach provides a clearer picture of the environment, allowing for better planning and resource allocation. For example, an organisation must conduct a risk assessment to determine market feasibility and address potential hurdles before launching a new product.

4. Ensure Compliance with Laws and Regulations: Risk management helps organisations adhere to legal, regulatory, and industry standards, reducing the risk of fines and legal actions. It identifies compliance risks and ensures that systems and processes meet the required standards. For example, a financial institution implements anti-money laundering (AML) procedures to comply with regulatory requirements.

5. Enhance Organisational Resilience: Risk management enhances an organisation’s resilience and capability to recover quickly from adverse events. It fosters resilience by preparing for disruptions and maintaining continuity of operations during crises. For example, businesses develop disaster recovery plans to ensure operations can continue during a natural disaster or cyberattack.

6. Increase Operational Efficiency: Risk management increases businesses’ operational efficiency by streamlining processes and reducing waste caused by unmanaged risks. It identifies inefficiencies, leading to optimised operations and better resource use. Hence, a company reduces downtime and improves overall productivity by identifying potential risks in production.

7. Protect Reputation and Brand Value: Risk management protects an organisation’s reputation and brand value. It helps maintain stakeholder trust and protects an organisation’s public image. Proactively managing risks can prevent scandals, negative publicity, and loss of customer confidence. For instance, a retail company recalls a defective product quickly to maintain customer trust and avoid reputational damage.

8. Seize Opportunities for Growth: Risk management helps organisations identify and capitalise on opportunities arising from calculated risks. Effective risk management balances risk and reward, enabling organisations to innovate while staying protected. For example, a company may diversify its investment portfolio after assessing the risks associated with different markets.

9. Facilitate Strategic Planning: Risk management facilitates strategic planning by aligning risk management with long-term organisational goals. It supports strategic decision-making by ensuring that risks to achieving objectives are understood and mitigated. For example, a global business must conduct geopolitical risk assessments before entering new international markets.

10. Promote a Risk-Aware Culture: Risk management facilitates a good risk-awareness culture, ensuring a proactive approach across all levels of the organisation. Risk-aware cultures encourage employees to identify and report risks, fostering a shared responsibility for risk mitigation. Regular risk management training ensures employees can handle risks effectively.

11. Achieve Financial Stability: Risk management helps organisations achieve financial stability, thereby enhancing their financial health. It ensures that unexpected costs are minimised and financial risks, such as credit and market risks, are managed effectively. For example, an organisation purchases insurance to cover liabilities and reduce the financial burden of unforeseen events.

Examples of Common Risks Businesses Face

Every business operates in a unique environment, but certain risks are universal across industries. By understanding what risk management is and recognising the types of risks that could affect their operations, businesses can begin building a resilient framework to protect their future. Here are some common categories of risks:

1. Financial Risk

Financial risks entail uncertainty regarding an organisation’s financial health, profitability, or cash flow. Causes of financial risk include market fluctuations, credit defaults, liquidity issues, and fund mismanagement.

Market risk arises from fluctuations in stock prices, interest rates, or currency exchange rates. Credit risk arises from customers or borrowers failing to repay loans. Liquidity risk arises from a company’s inability to meet short-term financial obligations due to insufficient cash. Financial Risk Mitigation Strategies include:

- Diversifying investments to reduce market exposure.

- Implementing robust credit assessment processes.

- Maintaining adequate cash reserves for liquidity.

2. Operational Risk

Operational risk arises from failures in internal processes, systems, people, or external events. Human errors, system breakdowns, fraud, supply chain disruptions, and natural disasters are common causes of operational risks. Examples of operational risks include:

- A factory halts production due to equipment failure.

- Errors in data entry leading to inaccurate financial reporting.

- Supply chain interruptions causing delivery delays.

Operational risk mitigation strategies include:

- Regular maintenance and updates for equipment and systems.

- Training programmes to reduce human errors.

- Establishing contingency plans for supply chain disruptions.

3. Strategic Risk

Strategic risk is associated with an organisation’s strategy or decision-making that impacts long-term goals and objectives. Causes of strategic risk include changes in market conditions, competitive pressures, poor strategic decisions, or failure to adapt to trends. Examples of strategic risks include:

- Entering a new market without adequate research.

- Launching a product that does not align with customer demand.

- Failing to adapt to technological advancements.

Strategic risk mitigation strategies include:

- Regular market analysis and competitor reviews.

- Aligning strategic goals with market trends and customer needs.

- Implementing a robust risk assessment framework for new initiatives.

4. Compliance Risk

Compliance risk arises from failing to adhere to laws, regulations, or internal policies, potentially leading to legal penalties, fines, or reputational harm. Causes of compliance risk include inadequate knowledge of regulations, ineffective compliance programs, or negligence. Examples of compliance risks include:

- Non-compliance with tax regulations resulting to penalities and fines.

- Breach of data protection laws like GDPR.

- Failure to meet industry-specific standards, such as ISO certifications.

Compliance risk mitigation strategies include:

- Implementation of robust compliance management systems

- Regular training staff on regulatory requirements

- Conducting compliance audits to identify and rectify gaps

5. Cybersecurity and Technology Risks

Cybersecurity and technology risks are associated with cyberattacks, data breaches, or technology failures affecting operations, security, or customer trust. Weak cybersecurity measures, outdated software, and inadequate IT governance are common causes of cybersecurity and technology risks. Examples of cybersecurity and technology risks include:

- A ransomware attack encrypts company data.

- Customer data theft due to weak network security.

- Downtime caused by IT system failures or outages.

Cybersecurity and technology risk mitigation strategies include:

- Implementing multi-layered cybersecurity measures (e.g., firewalls and encryption)

- Regular software updates and vulnerability assessments

- Developing and testing an incident response plan

6. Reputational Risk

Reputational risk is associated with damage to an organisation’s image, brand value, or stakeholder trust. Adverse publicity, ethical breaches and poor crisis management are key causes of reputational risks. Examples of reputational risk include:

- A product recall due to safety concerns damaging customer trust.

- Social media backlash over unethical business practices.

- Public scandals involving senior management.

Reputational risk mitigation strategies include:

- Proactively monitoring public sentiment and media coverage.

- Implementing ethical business practices and transparent communication.

- Developing a crisis management plan to address reputational threats effectively.

Why is Risk Management Important for Business?

Risk management is not just a protective measure but a strategic tool that enables businesses to navigate uncertainties, seize opportunities, and thrive in a competitive landscape. Without a well-structured risk management approach, companies may be vulnerable to avoidable disruptions, financial losses, and reputational damage.

Here are reasons why risk management is critical for businesses:

1. Protecting Business Assets and Reputation

- Financial Protection: Effective risk management safeguards a company’s tangible and intangible assets. For instance, having insurance coverage or a contingency fund ensures businesses can recover from financial losses caused by unforeseen events like natural disasters or market downturns.

- Reputational Protection: A single crisis, such as a data breach or unethical practice, can tarnish a brand’s reputation. Proactive risk management minimises such exposures, maintaining stakeholder trust.

2. Ensuring Operational Continuity

- Minimising Disruptions: Unexpected events can halt operations, from supply chain interruptions to power outages. A robust risk management strategy with contingency plans ensures businesses can continue functioning or recover quickly.

- Building Resilience: Businesses become more adaptable to environmental or market changes by identifying vulnerabilities and preparing for potential risks.

3. Supporting Strategic Decision-Making

- Informed Decisions: Risk management helps leaders better understand potential challenges, enabling more informed and calculated decision-making.

- Balancing Risks and Rewards: Not all risks are harmful; some present growth opportunities. For instance, expanding into a new market involves risks but can yield significant rewards if managed correctly.

4. Enhancing Stakeholder Confidence

- Reassuring Investors and Partners: Demonstrating a strong risk management framework signals to investors, lenders, and partners that the business is well-prepared and professionally managed.

- Building Employee Trust: Employees feel more secure working for an organisation that prioritises their safety and the stability of the business.

5. Compliance with Legal and Regulatory Requirements

- Avoiding Penalties: Many industries have stringent regulatory requirements. Effective risk management ensures compliance, reducing the risk of fines, legal actions, or shutdowns.

- Meeting Industry Standards: Implementing risk management best practices aligns businesses with globally recognised standards, enhancing credibility and market competitiveness.

6. Creating a Competitive Advantage

- Proactive Risk Identification: Businesses that identify and address risks before their competitors gain a significant advantage in the market.

- Driving Innovation: A well-managed approach to risk encourages businesses to innovate safely, exploring new technologies and processes without fear of catastrophic failure.

7. Ensuring Long-Term Sustainability

- Planning for the Future: Risk management is forward-looking, helping businesses anticipate challenges and adapt accordingly.

- Facilitating Growth: Companies with strong risk management frameworks are more likely to grow sustainably, as they can take calculated risks that support long-term objectives.

The Risk Management Process

The risk management process is a systematic approach to identifying, assessing, and addressing risks to minimise their impact on a business. Following a structured process, companies can proactively handle potential threats and opportunities, ensuring their operations run smoothly even when uncertainties arise. Let us highlight the key steps of an effective risk management process.

Step 1: Risk Identification

The first step in the risk management process is identifying the risks that could potentially affect the business. This stage systematically discovers all possible threats and vulnerabilities that might disrupt operations, affect resources, or damage the company’s reputation.

Risk Identification Techniques

There are several ways of identifying risks in an organisation, including:

- Brainstorming: Branstorm with stakeholders, employees, and industry experts to identify potential risks.

- SWOT Analysis: Conduct a SWOT (Strengths, Weaknesses, Opportunities, and Threats) analysis to uncover risks related to internal and external factors.

- Risk Checklists: Use pre-existing risk checklists or frameworks tailored to your industry to ensure all types of risks are considered.

- Historical Data Review: Review past incidents in the business, industry trends, or similar organisations to uncover recurring risks.

- Expert Consultations: Consult with specialists, such as legal advisors, financial experts, or industry consultants, to gain insights into less apparent risks.

Businesses can prepare more comprehensively for the unexpected by identifying various risks. See “100 Ways to Identify Risks in an Organisation” to learn more about risk identification techniques.

Step 2: Risk Assessment

Having identified potential risks, the next step is to assess them. Risk assessment involves evaluating the likelihood and impact of the identified risks to prioritise based on the level of attention and resources required to manage the risks. This helps businesses allocate resources effectively to address the highest-priority risks first.

Key Activities in Risk Assessment

By clearly understanding the magnitude of each risk, businesses can focus on risks that pose the most significant threat to their goals and operations. Here are key activities in risk assessment:

- Risk Likelihood: Estimate the likelihood of each risk. Based on available data or expert judgment, this can be categorised as “Low,” “Medium,” or “High.”

- Risk Impact: Assess each risk’s potential consequences or severity for the business. These may include financial loss, reputational damage, or operational disruption.

- Risk Matrix: Use a risk matrix (also known as a risk heat map) to visually plot the likelihood and impact of risks on a scale (e.g., low, medium, high). This helps prioritise the most critical risks.

- Qualitative vs. Quantitative Assessment: Qualitative assessment uses subjective judgment, while quantitative assessment involves numerical data, e.g., financial projections and probability analysis, to evaluate risks.

- Scenario Planning: Consider different scenarios and potential outcomes for more significant risks to understand the consequences.

Step 3: Risk Mitigation

After assessing the risks, the next step is to mitigate them – i.e., implement strategies to reduce the likelihood or impact of the identified risks. Risk mitigation involves both preventive measures to avoid risks and contingency plans to respond to them when they occur.

Key Risk Mitigation Strategies

- Risk Avoidance: Altering plans or processes to avoid risk altogether, e.g., avoid entering a market with high regulatory uncertainty.

- Risk Transfer: Shifting the responsibility or financial burden of a risk to a third party, such as through insurance, outsourcing, or contractual agreements. For example, purchasing cyber insurance to protect against data breaches.

- Risk Reduction: Implementing measures to reduce the likelihood or severity of a risk. This could involve safety protocols, employee training, regular equipment maintenance, or security upgrades.

- Risk Acceptance: In some cases, accepting a risk may be more cost-effective, especially if the likelihood or impact is low. In such cases, businesses may prepare by setting aside a reserve fund or having a contingency plan.

Step 4: Risk Monitoring and Review

Risk management is an ongoing process, and risks can evolve. The final step is to monitor the identified risks and review the effectiveness of mitigation strategies regularly. Risk monitoring ensures that the risk management framework remains responsive to changing circumstances and that the business is prepared for new or emerging risks. Monitoring ensures that a business promptly and effectively addresses new risks to minimise disruptions.

Key Activities in Monitoring and Review

- Regular Monitoring: Continuously track key risk indicators and adjust as needed. This could include tracking regulation changes, market conditions, or internal performance metrics.

- Risk Audits: Conduct periodic audits to evaluate the effectiveness of risk management strategies and whether new risks have emerged.

- Feedback Loops: Establish feedback mechanisms to gather input from employees, customers, and other stakeholders on the effectiveness of risk management efforts.

- Post-Incident Reviews: This entails conducting a detailed review of an incident after it occurs to assess how well the business handled the situation and what could be improved.

- Adjustments and Updates: Regularly updating risk assessments and mitigation strategies to address new risks and changes in the business environment.

The risk management process is essential for any business aiming to thrive in an uncertain world. Companies can protect their assets, ensure operational continuity, and build long-term resilience by systematically identifying, assessing, mitigating, and monitoring risks. The process is not a one-time effort but an ongoing strategy that adapts to the changing landscape of risks and opportunities.

Risk Management Tools and Techniques

Businesses can use various tools and techniques to identify, assess, mitigate, and monitor risks effectively to implement risk management. These tools help provide structure, improve decision-making, and ensure that risks are managed systematically and effectively. Let’s explore some of the most common and widely used risk management tools and techniques.

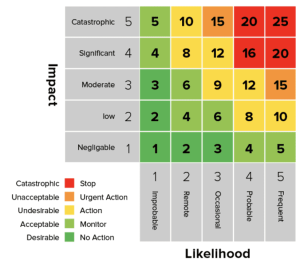

1. Risk Heat Map (Risk Assessment Matrix)

A Risk Heat Map (or Risk Assessment Matrix) is a visual tool for assessing and prioritising risks based on their likelihood and impact. It is essential for providing a clear, easy-to-understand overview of business risks for well-informed decision-making. This is a good corporate risk management practice. Here is a risk heat map.

How Risk Heat Map Works

- Risks are plotted on a grid that categorises them based on the likelihood of occurrence (e.g., low, medium, high) and the severity of their impact (e.g., low, medium, and high).

- Risks in the “high likelihood/high impact” quadrant are prioritised, while those in the “low likelihood/low impact” quadrant may be deprioritised.

Advantages of Risk Heat Map Works

- Helps businesses quickly identify critical risks that need immediate attention.

- Provides an accessible, straightforward way to communicate risk priorities to stakeholders.

2. Failure Mode and Effect Analysis (FMEA)

Failure Mode and Effect Analysis (FMEA) is a structured technique for evaluating potential failures within a process or system. It helps businesses understand how and why a particular failure might occur and its possible effects on the organisation.

How FEMA works

- List all possible failure modes in a process or system.

- Assess the likelihood, severity, and detectability of each failure.

- Multiply the likelihood, severity, and detectability scores to assign each failure mode a risk priority number (RPN).

- Prioritise failure modes with the highest RPN for corrective actions.

Advantages of FEMA

- A proactive approach to identifying potential process failures before they occur.

- Facilitates systematic prioritisation of risks based on severity and probability.

3. Monte Carlo Simulation

The Monte Carlo Simulation is a mathematical modelling technique used to understand the impact of uncertainty and variability on decision-making. It uses random sampling and statistical analysis to simulate possible outcomes for a particular risk or project.

How Monte Carlo Simulation Works

- Input a set of variables (e.g., financial data, project costs, market conditions) that are subject to uncertainty.

- The simulation runs multiple trials, producing a distribution of possible outcomes based on the probability of various inputs.

- The result is a comprehensive picture of the potential range of outcomes and the likelihood of each.

Advantages of Monte Carlo Simulation

- Provides a probabilistic range of outcomes, allowing businesses to make more informed decisions.

- Helps forecast future trends and assess the impact of risks over time.

4. Risk Registers

A risk register is a centralised document or tool that tracks all identified risks, their assessments, and their actions to address them. It is a crucial tool for risk management, particularly in complex organisations where risks may arise across multiple departments or projects.

How it Works

- The risk register includes columns for risk descriptions, likelihood, impact, mitigation strategies, owners, and timelines for mitigation actions.

- It must be updated regularly to capture new risks, their status, and any adjustments made to mitigation strategies.

Advantages of Risk Register

- Keeps all stakeholders informed and aligned on risk management efforts.

- Acts as a reference for decision-making and continuous improvement in the risk management process.

5. SWOT Analysis (Strengths, Weaknesses, Opportunities, and Threats)

SWOT Analysis is a strategic planning tool commonly used to assess internal and external factors that could impact the organisation, including opportunities and risks. It helps businesses identify their strengths, weaknesses, external opportunities, and threats.

How SWOT Works

- Strengths: Identify internal factors that give the organisation a competitive advantage.

- Weaknesses: Highlight internal limitations or areas where the organisation may be vulnerable.

- Opportunities: Assess external factors that could present growth or improvement opportunities.

- Threats: Identify external risks and challenges that could negatively affect the organisation.

Advantages of SWOT

- Provides a comprehensive overview of internal and external risks.

- It helps businesses align their risk management strategies with their broader strategic goals.

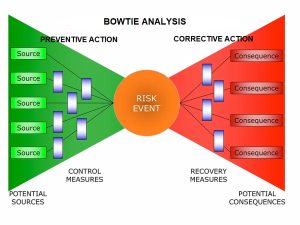

6. Bowtie Diagram

A Bowtie Diagram is a visual tool representing the cause-and-effect relationships between risks and their consequences. It is beneficial for illustrating how various risk factors can lead to specific outcomes and the controls in place to mitigate those risks.

How it works:

- The diagram is shaped like a bowtie, with the “knot” in the centre representing the risk event (as shown above).

- The left side of the bowtie represents the causes of the risk event (what leads to the risk), while the right side represents the consequences (the impacts of the risk).

- Control measures or mitigations are placed between the causes and consequences to show how they can prevent or reduce the risk.

Advantages of Bowtie Diagram

- Provides a visual representation of risk and its management.

- Clarifies the relationship between causes, consequences, and controls, making understanding and communicating risk easier.

7. Risk Scoring and Ranking

Risk Scoring and Ranking involve assigning numerical values to various aspects of risk, such as its likelihood and impact, and using these scores to prioritise risks. This technique is proper when a company has many risks and needs a systematic way to rank them based on severity.

How Risk Scoring and Ranking Works

- Assign a numerical value to the likelihood (e.g., 1 to 5, where 1 is rare and 5 is almost inevitable).

- Assign a numerical value to the impact (e.g., 1 to 5, where 1 is negligible and 5 is catastrophic).

- Multiply the likelihood score by the impact score to obtain a risk score.

- Rank risks from highest to lowest based on their risk scores.

Advantages of Risk Scoring and Ranking

- It provides a quick way to prioritise risks.

- It enables businesses to focus resources on the most critical risks first.

8. Decision Trees

A Decision Tree is a graphical tool that helps businesses make decisions by mapping out possible outcomes based on various risk scenarios. It is suitable for evaluating complex decisions that involve uncertainty and multiple potential outcomes.

How Decision Tree works

- Start with a decision node that represents the primary decision.

- Branch out to different possible outcomes, each with associated probabilities.

- Continue branching out based on possible future decisions and their outcomes.

- Assign monetary values or other relevant measures to each potential outcome and calculate the expected value.

Advantages of Decision Tree

- It helps businesses visualise the impact of various decision pathways.

- Provides a structured framework for evaluating multiple options and their risks.

Real-Life Examples of Risk Management in Action

Understanding how risk management is applied in real-world scenarios can provide valuable insights into its practical use and effectiveness. Businesses use different approaches to handle risks and protect their operations. Here are real-life examples highlighting diverse applications of risk management strategies.

1. Toyota’s Approach to Supply Chain Risk Management

Industry: Automotive

Risk: Supply Chain Disruption

In 2011, a devastating earthquake and tsunami hit Japan, severely disrupting the supply chain for many businesses, including Toyota. The automotive giant faced significant challenges as key suppliers could not deliver essential parts. This event exposed vulnerabilities in their supply chain, primarily concentrated in specific geographic regions and suppliers.

Risk Management in Action:

- Diversification and Resilience: Toyota’s response to this crisis was to increase the resilience of its supply chain. They shifted from relying on a small number of suppliers in specific regions to a more diversified supply chain model that spreads risk across various suppliers and geographic locations.

- Just-in-Case Strategy: In contrast to the “Just-in-Time” (JIT) production system that focuses on minimising inventory, Toyota adopted a “Just-in-Case” strategy, building buffer stock of critical components to ensure operations would not be halted in case of future disruptions.

- Enhanced Supplier Relationships: Toyota strengthened relationships with suppliers, emphasising the need for contingency planning and creating a risk-sharing framework.

Outcome: These strategies helped Toyota mitigate the effects of future supply chain disruptions and improve its long-term resilience, making it less vulnerable to similar risks.

2. BP’s Risk Management after the Deepwater Horizon Disaster

Industry: Oil & Gas

Risk: Environmental and Operational Risk

In 2010, BP faced one of the most catastrophic oil spills in history after the Deepwater Horizon rig exploded, causing millions of barrels of oil to spill into the Gulf of Mexico. The event led to significant environmental damage, loss of human lives, regulatory fines, and long-term reputational damage.

Risk Management in Action:

- Root Cause Analysis and Risk Assessment: Following the disaster, BP conducted extensive risk assessments to understand the root causes of the explosion and identify areas of vulnerability in their operations. This involved evaluating the safety procedures, equipment failures, and the adequacy of risk management strategies at the time.

- Safety and Environmental Improvements: BP implemented stricter safety and environmental regulations, including enhanced sound pressure monitoring systems and blowout preventers. They also established a new safety culture, emphasising risk assessments and ensuring that safety considerations were integrated into all phases of their operations.

- Crisis Management and Communication: BP improved its crisis management systems, ensuring faster and more effective responses to operational incidents. Additionally, BP significantly overhauled its communication protocols to provide better engagement with stakeholders and the public.

Outcome: BP’s response to the Deepwater Horizon disaster highlighted the importance of continuous risk management and learning from past failures. They implemented better safety measures and adopted a proactive approach to preventing future environmental risks.

3. Facebook’s Data Privacy and Security Risk Management

Industry: Technology (Social Media)

Risk: Data Privacy and Security Breach

In 2018, Facebook was embroiled in a major data privacy scandal when third-party firms harvested and misused the personal data of millions of users, including the infamous Cambridge Analytica incident. This scandal raised significant concerns about Facebook’s ability to protect user data and raised legal and regulatory risks.

Risk Management in Action:

- Data Protection and Compliance Upgrades: Facebook responded by implementing stricter data protection and privacy protocols in line with global standards such as the General Data Protection Regulation (GDPR). They introduced enhanced user privacy settings, data encryption measures, and tools to give users more control over their data.

- Third-Party Risk Management: Facebook also strengthened its third-party risk management, placing stricter guidelines on how external developers could access and use user data. They also implemented regular audits and monitoring processes to ensure compliance with their data protection policies.

- Public Communication and Reputation Management: Facebook took active steps to rebuild its public reputation by increasing transparency regarding its data handling practices, publicly addressing the Cambridge Analytica issue, and engaging with regulators to mitigate future risks.

Outcome: While the scandal severely impacted Facebook’s reputation in the short term, its risk management response helped the company regain user trust and align with evolving global data protection regulations. These actions demonstrated a commitment to safeguarding user privacy and reducing future risks.

4. Apple’s Product Quality Control and Reputation Risk Management

Industry: Technology (Consumer Electronics)

Risk: Product Quality and Consumer Satisfaction

In 2010, Apple faced significant criticism when its flagship product, the iPhone 4, was found to have a design flaw. The issue, commonly referred to as “Antennagate,” involved the device’s antenna performance, which caused signal drop issues when held in a certain way. This posed a risk to the company’s reputation for delivering high-quality products.

Risk Management in Action:

- Immediate Response and Product Recall: Apple’s risk management team quickly addressed the issue by offering affected customers free bumper cases to mitigate the antenna issue. They also allowed customers to return the phone for a full refund if dissatisfied with the product’s performance.

- Transparent Communication: Apple’s CEO, Steve Jobs, held a public press conference to address customers’ concerns directly, assuring them that the company was committed to delivering the best possible products and addressing any quality issues.

- Design Improvements and Product Testing: Apple revamped its product testing procedures, emphasising more comprehensive quality assurance processes to ensure that future products would not have similar issues. They also improved the antenna design in future iPhone models.

Outcome: By swiftly addressing the issue and taking responsibility for the product flaw, Apple managed the crisis and minimised long-term damage to its brand. The company continued to innovate and maintain customer loyalty, reaffirming its commitment to product quality.

5. Amazon’s Cybersecurity Risk Management

Industry: E-Commerce & Cloud Computing

Risk: Cybersecurity and Data Breach

As one of the world’s largest online retailers and cloud service providers, Amazon faces constant risks related to cybersecurity, mainly due to the vast amounts of customer data it handles. The company has experienced several high-profile security breaches over the years, and its risk management strategy is continually evolving to address the growing sophistication of cyberattacks.

Risk Management in Action:

- Proactive Monitoring and Threat Detection: Amazon uses advanced machine learning algorithms and artificial intelligence (AI) to detect potential security threats and breaches in real-time. The company monitors its network for unusual activity and suspicious behaviour, enabling it to take immediate action to prevent cyberattacks.

- Cloud Security Enhancements: Amazon Web Services (AWS) has invested heavily in state-of-the-art cybersecurity infrastructure, such as end-to-end encryption, multi-factor authentication, and strong access controls, to protect both its customers and its data.

- Employee Training and Awareness: Amazon regularly trains its employees on cybersecurity best practices to reduce the risk of internal threats, such as phishing attacks or data leaks.

Outcome: Through these ongoing investments in cybersecurity, Amazon has safeguarded its vast network of users and prevented many potential data breaches. This robust risk management framework helps maintain customer trust, a critical factor for the company’s continued success.

These real-life examples illustrate how organisations across various industries approach risk management. Whether responding to natural disasters, operational failures, security breaches, or reputational damage, businesses use a combination of proactive strategies, real-time monitoring, and continuous improvement to protect themselves and their stakeholders. By understanding and learning from these examples, an organisation can better prepare for risks and ensure they are well-positioned to navigate uncertainty.

Practical Tips for Implementing Risk Management in an Organisation

Effective risk management protects an organisation against unforeseen challenges, enables growth, and enhances decision-making. Implementing a structured risk management strategy can seem overwhelming, especially for small or mid-sized businesses. However, businesses can integrate risk management into their day-to-day operations with a practical approach and the right tools. Here are practical tips to help businesses implement risk management successfully:

1. Understand Business Risks

Identifying and analysing risks is essential to ensuring sound business risk management. Risks arise from several sources, including operational, financial, strategic, regulatory, and environmental.

Practical Steps:

- Conduct a Risk Assessment: Conduct a thorough risk assessment to identify potential threats. This can involve brainstorming sessions with key stakeholders, reviewing historical data, and considering industry-specific risks.

- Use a Risk Register: Create a risk register that logs all identified risks, their potential impact, and the likelihood of occurrence. This tool helps businesses track risks over time and prioritise them based on severity.

- Risks must be categorised into groups (e.g., financial, operational, legal, environmental, and reputational) to ensure comprehensive coverage.

2. Prioritise Risks Based on Impact and Likelihood

Not all risks are equal. Some risks can cause significant damage to an organisation, while others may have a minimal impact. Risk prioritisation ensures resource allocation to the most critical threats.

Practical Steps:

- Use a Risk Matrix: A risk matrix or heat map can be used to visually assess the likelihood and impact of each identified risk. This helps you rank risks from most to least critical.

- Assess Risk Tolerance: Understand the level of risk an organisation is willing to accept. This helps decide which risks to mitigate, accept, or transfer.

- It is crucial to first focus on high-impact and high-likelihood risks that may disrupt business operations, followed by medium-likelihood risks with moderate effects.

3. Develop a Risk Management Plan

A risk management plan outlines the steps to mitigate, manage, or accept the identified risks. A clear plan ensures that everyone understands their roles and responsibilities when managing risks.

Practical Steps:

- Identify Mitigation Strategies: For each prioritised risk, determine actions to mitigate or eliminate the threat. This includes implementing new policies, purchasing insurance, and building contingency plans.

- Create Contingency Plans: Develop backup plans for critical business areas (e.g., supply chain disruptions, data breaches). Ensure these plans are practical, easy to implement, and well-communicated to key stakeholders.

- Assign Roles and Responsibilities: Ensure that individuals or teams are accountable for managing specific risks. This promotes responsibility and streamlines the risk management process.

- Businesses must regularly update their risk management plan to reflect environmental changes and manage emerging risks.

4. Implement Risk Controls and Mitigation Measures

Having identified potential risks and developed a risk management plan, it is time to implement specific controls to mitigate them. Depending on the risk involved, risk controls can take many forms.

Practical Steps:

- Operational Controls: Implement procedural changes or safeguards that reduce operational risks (e.g., double-checking financial transactions and automating routine tasks to reduce human error).

- Financial Controls: Protect against financial risks by using insurance, diversifying investments, and maintaining a robust cash flow management system.

- Technological Controls: Use cybersecurity tools, firewalls, encryption, and regular software updates to protect against data breaches and system failures.

- Compliance Measures: To avoid legal and regulatory risks, ensure your business complies with relevant regulations (e.g., GDPR and OSHA).

- Create a culture of risk awareness within an organisation. Encourage employees to report potential risks and take proactive risk mitigation measures.

5. Regularly Monitor and Review Risks

Risk management is an ongoing process. Regular monitoring ensures that a business can adapt to new challenges, track the effectiveness of its risk mitigation strategies, and take corrective action if necessary.

Practical Steps:

- Review and Update the Risk Register: Review the risk register to identify and prioritise new risks. This is necessary to eliminate unnecessary risks and manage emerging risks.

- Monitor Key Risk Indicators (KRIs): Track metrics that provide early warning signs of risks. For example, if the business relies heavily on a single supplier, monitor their financial health or delivery performance.

- Conduct Regular Audits: Conduct audits and assessments to evaluate the effectiveness of the risk management strategies. This could include financial audits, security audits, or process reviews.

- Schedule regular risk management reviews, such as quarterly or semi-annual risk meetings, to discuss new risks and ensure ongoing compliance.

6. Leverage Technology to Support Risk Management

In today’s digital age, businesses can use various software tools and platforms to streamline risk management processes. Technology helps organisations monitor, analyse, and mitigate risks in real-time to improve their risk management framework.

Practical Steps:

- Risk Management Software: Consider using specialised risk management software to track and analyse risks, automate assessments, and maintain an up-to-date risk register.

- Data Analytics: Data analytics can identify emerging trends and patterns that could indicate potential risks. This can be particularly useful for financial risks, market shifts, or customer behaviour changes.

- Cloud Solutions: Cloud-based platforms allow businesses to back up critical data and protect against system failures or cyberattacks.

- Invest in technology that integrates with existing systems and provides real-time insights into a business risk landscape.

7. Engage Stakeholders in Risk Management

Risk management should not be siloed; engaging various stakeholders is crucial. Including the company’s management team, board of directors, customers, suppliers, and other relevant parties ensures a comprehensive approach to risk management.

Practical Steps:

- Communicate Risk Management Strategies: Regularly communicate the company’s risk management strategies and updates to key stakeholders. Transparency fosters trust and collaboration.

- Create a Risk Culture: Encourage employees at all levels to take ownership of risk management. Offer training and resources to help them identify and manage risks effectively.

- Collaborate with External Partners: Work closely with the company’s suppliers, contractors, insurers, and consultants to identify shared risks and develop joint mitigation strategies.

- Dialogue with Internal Stakeholders: Encourage open dialogue about risks across the organisation. Create an environment where employees feel empowered to identify and discuss risks without fear of blame.

8. Continuously Improve the Business Risk Management Strategy

The business environment is dynamic, and risks evolve. Therefore, it is essential to continuously improve risk management practices based on past experiences, feedback, and changes in the external environment.

Practical Steps:

- Learn from Past Incidents: When a risk event occurs, conduct a post-mortem analysis to understand what went well and what could have been done better. The findings and observations must be used to improve future risk strategies.

- Adapt to Industry Changes: Stay informed about industry trends and changes, including regulatory updates, technological advancements, and shifts in market conditions.

- Promote Ongoing Training: Regularly train the business team on the latest risk management practices, tools, and technologies to ensure they can handle evolving risks.

- Engage employees and other stakeholders regularly for feedback on improving risk management processes. Incorporating feedback fosters a culture of continuous improvement.

Prioritising Risk Management in Business Operations

Risk management is a cornerstone of successful business operations. It ensures that potential challenges are addressed proactively to maintain stability, foster growth, and safeguard resources. Prioritising risk management in daily operations enables organisations to operate confidently, resiliently, and efficiently.

Why Prioritising Risk Management in Business Operations?

1. Protect Organisational Assets: Businesses face various risks, including financial losses, operational disruptions, or reputational damage. Risk management safeguards these assets and ensures the continuity of operations.

2. Enhance Decision-Making: A structured approach to managing risks provides critical insights, enabling better strategic decisions and resource allocation.

3. Maintain Regulatory Compliance: Prioritising risk management helps organisations adhere to legal and industry standards, reducing the likelihood of penalties or legal actions.

4. Foster Resilience: Effective risk management equips organisations to recover quickly from disruptions, ensuring long-term sustainability.

5. Build Stakeholder Confidence: Demonstrating robust risk management practices reassures customers, investors, and partners of the organisation’s stability and reliability.

Steps to Prioritising Risk Management in Business Operations

1. Develop a Risk-Aware Culture:

- Educate employees at all levels about the importance of identifying and addressing risks.

- Encourage proactive risk reporting and collaboration.

2. Integrate Risk Management into Strategic Planning:

- Align risk management practices with organisational goals.

- Incorporate risk assessments into project planning and decision-making processes.

3. Identify and Assess Risks:

- Regularly identify potential financial, operational, strategic, and technological risks.

- Evaluate the likelihood and impact of each risk to prioritise action.

4. Implement Risk Mitigation Measures:

- Design strategies based on the assessment to minimise, transfer, or accept risks.

- For example, invest in cybersecurity to prevent data breaches or diversify suppliers to mitigate supply chain disruptions.

5. Monitor and Review Risks Continuously:

- Establish systems to track risks in real time, adapting strategies as new threats emerge.

- Regularly review risk management plans to ensure effectiveness.

6. Leverage Technology for Risk Management:

- Use risk management software to streamline identifying, monitoring, and mitigating risks.

- Employ data analytics to gain deeper insights into potential vulnerabilities.

7. Engage Stakeholders:

- Keep stakeholders informed about risks and the steps taken to manage them.

- Collaborate with external partners, such as insurers or consultants, to enhance risk management efforts.

Examples of Prioritising Risk Management

1. Manufacturing Sector:

- Identifying risks of equipment failure and scheduling preventive maintenance to minimise downtime.

- Mitigating supply chain risks by diversifying suppliers and securing alternative logistics routes.

2. Financial Services:

- Ensuring compliance with evolving regulatory requirements to avoid fines and maintain trust.

- Implementing fraud detection systems to protect assets and customer data.

3. Retail and E-commerce:

- Managing reputational risks by addressing customer complaints promptly and transparently.

- Preventing cybersecurity risks by securing payment gateways and protecting sensitive data.

Benefits of Prioritising Risk Management

- Operational Continuity: Minimised disruptions ensure smooth operations.

- Financial Stability: Reduced financial losses from unforeseen events.

- Competitive Advantage: A reputation for reliability and resilience sets businesses apart.

- Increased Efficiency: Proactively addressing risks leads to streamlined processes and resource optimisation.

Conclusion

Risk management is a critical yet often overlooked component of successful business operations. This article has explored the fundamentals of risk management and the need to master It. It outlines essential steps to protect a business in the modern business terrain.

To recap, here are the key takeaways:

- Risk Management: It involves identifying, assessing, and mitigating potential risks that could negatively impact business operations. It helps safeguard the business and promotes strategic decision-making.

- The Importance of Risk Management: Effective risk management allows businesses to anticipate challenges, minimise disruptions, and protect assets and reputations. It also helps maintain financial stability and regulatory compliance.

- Risk Management Process: The process includes identifying risks, assessing their impact and likelihood, prioritising them, and implementing strategies to mitigate or transfer risks. Continuous monitoring and review are essential for adapting to changing circumstances.

- Risk Management Tools and Techniques: Businesses can manage risk using various tools, such as risk registers, risk matrices, insurance, and contingency plans. Each tool serves a specific purpose and should be tailored to the type of risk faced.

- Practical Tips for Implementation: Effective implementation of risk management requires understanding business risks, developing a comprehensive risk management plan, and ensuring regular monitoring and feedback. Involving key stakeholders and leveraging technology can further streamline the process.

- Real-Life Examples: The best way to learn is through real-world examples. We highlighted how major companies like Toyota and BP effectively managed crises and the lessons learned from their experiences. Such cases demonstrate that proper risk management can help mitigate potential losses and create resilience.

- Prioritise Risk Management in Business Operations: Prioritising risk management in business operations is a defensive strategy and a proactive approach to building a robust, agile, and sustainable organisation. By embedding risk management practices into the core of operations, businesses can navigate uncertainties effectively, seize opportunities confidently, and thrive in a dynamic environment.

The business landscape is inherently unpredictable, and risks are inevitable. However, prioritising risk management in business operations ensures the company is well-equipped to handle uncertainty and disruptions. Risk management must be integrated into organisations’ (small businesses and large corporations) strategic planning and decision-making processes.

Now is the time to take control of the risks affecting a business. Start by assessing the business risk landscape, building a solid risk management plan, and involving key stakeholders. Don’t wait until a crisis strikes; be proactive and set the business up for long-term success.

If you’re unsure where to start or need professional guidance, seeking help from a risk management expert can be incredibly valuable. A consultant or coach can assist in developing a customised plan tailored to the business’s unique risks. Risk management coaching helps enhance the risk management capability of business owners and managers.

To enhance your knowledge of risk management, consider getting “Mastering Risk Management and Enterprise Risk Management (A Comprehensive Guide)”.

For more in-depth resources on risk management, visit the Institute of Risk Management (IRM) and Risk Management Society (RIMS). These leading global organisation provides expert insights, tools, and training for risk management professionals.